You found out your loft has spray foam insulation. Maybe a surveyor flagged it. Maybe your estate agent mentioned it. Maybe your mortgage application just got refused.

Now you are wondering: is this actually as bad as they are saying?

The honest answer is yes – and this guide explains exactly why, which banks are saying no, and what your options are right now.

Why Do Banks Care About Spray Foam?

Banks do not lend money on guesswork. Before approving any mortgage, they send a qualified surveyor to inspect the property and confirm it is structurally sound and worth what they are lending against it.

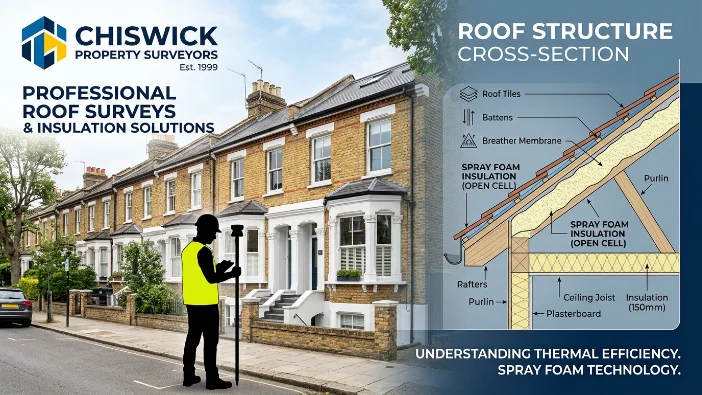

Here is the problem with spray foam: it covers everything.

When spray foam is applied to the underside of roof tiles and rafters, it creates a solid layer that completely hides the timber structure underneath. The surveyor cannot see the rafters. They cannot check for rot, decay, woodworm, or water damage. They cannot confirm the roof is in the condition it needs to be in.

No inspection means no certainty. No certainty means no mortgage.

Surveyors appointed by mortgage lenders find it impossible to inspect the roof structure when spray foam is present — the foam conceals the very timbers, tiles, and membranes they need to examine.

It is not personal. It is not the bank being difficult. It is a straightforward risk decision — and they almost always come down on the side of caution.

Which Banks Refuse Mortgages on Spray Foam Properties?

This is the part most homeowners want to know. The list is long.

Halifax declines mortgages on spray foam properties, with surveyors flagging it as a defect that prevents timber inspection. Nationwide will not lend on properties with spray foam applied directly to roof timbers. Barclays rejects applications where spray foam is present in the roof space. NatWest and RBS have a standard policy to decline spray foam properties. Santander generally refuses lending on spray foam insulated properties.

Research across UK mortgage providers found that the vast majority — including most high street banks and virtually all equity release lenders — will not lend on properties with spray foam insulation in the roof.

In total, over 50 major UK lenders now have policies that flag or refuse spray foam properties. This includes most high street banks and virtually every equity release provider in the country.

A small number of specialist lenders may consider applications — but they typically require costly additional surveys, charge higher rates, and many still decline at the end of the process.

What About Equity Release?

Even worse than mortgages.

If you were planning to release equity from your home to fund retirement, home improvements, or care costs, spray foam insulation is almost certainly going to block that too. Equity release lenders are even more cautious than standard mortgage lenders, and the vast majority will not lend on a property where spray foam is present — regardless of how well it was installed.

How Many UK Homes Are Affected?

Over 250,000 UK homes are potentially affected by spray foam mortgage restrictions.

Most of these installations happened between 2016 and 2022, when spray foam was actively promoted — and in some cases funded — under government energy efficiency schemes including the Green Homes Grant and the ECO4 scheme.

The ECO4 grant and Great British Insulation Scheme both fund the installation of spray foam to eligible households — which is why so many homeowners feel particularly let down. They followed the advice, took the grant, and are now left with a bill to undo it.

In March 2025, the government confirmed that there is no government financial assistance for homeowners to have spray foam insulation removed.

What Happens When a Sale Falls Through?

This is where it gets painful.

Imagine you accept an offer on your home. Solicitors are instructed. The buyer gets a mortgage survey done. The surveyor flags the spray foam. The buyer’s lender refuses to lend. The sale collapses.

This is happening to UK homeowners every week. Estate agents, surveyors and other property professionals are increasingly likely to raise concerns if you have spray foam, with some estate agents refusing to list properties with the insulation installed.

Even if a buyer offers to purchase with cash to avoid the mortgage problem, they know you are limited in who you can sell to — and they will almost certainly use that as leverage to push your price down significantly.

Does Spray Foam Actually Damage the Roof?

This is a fair question, and the answer depends on what type of foam you have and how it was installed.

Open-cell foam is softer and more breathable. It is less likely to trap moisture, but it still prevents inspection — which is enough for most lenders to refuse.

Closed-cell foam is the more serious one. It is rigid, completely airtight, and bonds tightly to tiles and timbers. Closed-cell spray foam prevents natural ventilation, trapping condensation against roof timbers and accelerating decay. It also bonds to roof tiles, preventing individual tile replacement and turning a simple repair into a full roof strip.

The Property Care Association and Home Owners Alliance found that 35% of properties inspected had at least one defect caused by spray foam insulation, based on inspections at over 500 properties.

So while not every home with spray foam has active damage, a significant number do — and the ones that do not yet have damage may develop it over time.

Can You Sell a House With Spray Foam?

You can try — but your options are limited.

Without removal, you are effectively limited to cash buyers. That means a much smaller pool of potential buyers. And those buyers know exactly the situation you are in. Expect lower offers and longer time on the market.

If you want to sell at full market value, to any buyer, with a standard mortgage — removal is the only route.

What Is the Solution?

Professional spray foam removal, done by qualified specialists, restores your roof structure to a condition that surveyors and lenders can work with.

After removal, you receive documentation confirming the work has been carried out. This is what your lender, surveyor, or estate agent will need to see before proceeding.

At Spray Foam Removal UK, we help homeowners across the UK go from unmortgageable to mortgage-ready. You can find out exactly what our spray foam removal service involves — the process is straightforward:

- Start with a free online estimate so you know what the cost looks like

- We assess your property and confirm the foam type and coverage

- Our specialist contractors remove the foam cleanly and safely

- You receive written documentation to support your mortgage or sale

FAQs

Will removing spray foam definitely get my mortgage approved?

In most cases, yes – professional removal with the correct documentation allows lenders to reassess. However, lender decisions are always their own, and individual circumstances vary. We can confirm what documentation your lender is likely to need.

How long does the whole process take?

Most removal jobs take 2 to 5 days. Once complete, documentation is issued promptly so you can move forward with your mortgage or sale without unnecessary delays.

My spray foam was installed under a government scheme – is anyone responsible?

The government’s position is that homeowners should seek redress from their installer first. If that route is not available, you may have options through TrustMark or an insurance-backed guarantee if one was issued at the time of installation. In practice, many homeowners find these routes difficult and end up paying for removal themselves.

Can I just get a specialist survey instead of removing it?

Some lenders will consider a specialist survey report before making a decision. However, many still require removal regardless. If your lender has already refused, removal is almost always the only path forward.

What happens to the loft after removal?

The loft will need re-insulating with a lender-approved alternative – mineral wool rolls or PIR boards are the most common choices. These are breathable, mortgage-friendly, and typically cheaper than the spray foam was to install.

Spray foam does not have to be the end of your sale or mortgage application.

Most of our customers get a quote within 24 hours. No obligation, no pushy sales calls — just a clear picture of what removal involves and what it costs.