If you have spray foam insulation in your Hampshire property, the most important question right now is simple: will your mortgage lender accept it?

The short answer is: most will not. Here is exactly what you need to know.

Why Mortgage Lenders Refuse Spray Foam Properties

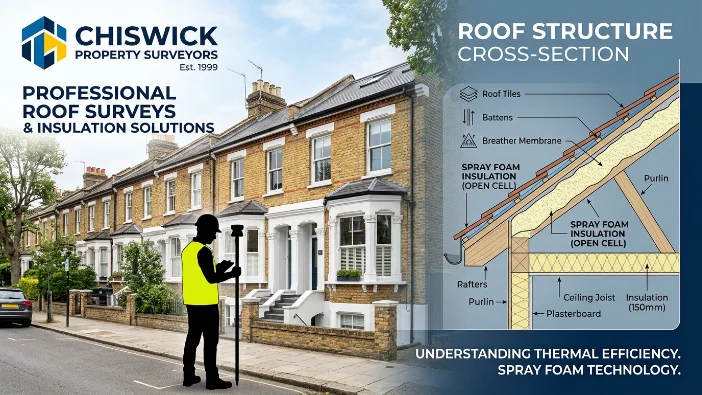

Spray foam insulation covers your roof timbers completely. When a mortgage surveyor visits your property, they cannot inspect the timber underneath the foam — they cannot see whether it is rotting, damp, or structurally sound.

For a lender, this is a problem. They are lending hundreds of thousands of pounds against your property. If they cannot verify the roof structure is in good condition, most will simply refuse to lend.

It is not about the foam itself. It is about what the foam is hiding.

Which Lenders Will Refuse Your Hampshire Mortgage

These lenders will refuse or flag a mortgage application on a Hampshire property with spray foam insulation:

Lenders With a Complete Ban

TSB has the strictest policy of any mainstream lender — it will not lend on any property where spray foam is present in the roof space, regardless of foam type, age, installation quality, or any documentation provided.

Lenders That Flag and Typically Refuse

Halifax, Nationwide, Barclays, NatWest, Santander, Skipton Building Society, and Leeds Building Society all flag spray foam during the valuation process. In the vast majority of cases, they issue a mortgage retention or outright refusal until professional removal and a completion certificate are provided.

This covers the majority of Hampshire homebuyers and remortgagors. If your buyer is using any of these lenders — which most buyers are — your sale will stall unless the foam is removed.

Equity Release Lenders

Every equity release lender in the UK will refuse a property with spray foam insulation. There are no exceptions. If you are a Hampshire homeowner looking to release equity and spray foam is present, removal is the only path forward.

Which Lenders Might Consider It

A very small number of specialist lenders will consider spray foam properties under specific conditions:

- The foam must be open-cell, not closed-cell

- It must have been installed with a current BBA or KIWA certificate

- The original installation paperwork must be available

- A specialist PCA-registered surveyor must confirm low-risk status

In practice, most Hampshire homeowners cannot meet all of these conditions — particularly the paperwork requirement, since many installations during the 2000s grant schemes were carried out without proper documentation being passed to the homeowner.

Even where conditions are met, specialist lenders typically offer higher interest rates and stricter terms. Most Hampshire homeowners who go through this process find that professional removal is faster, cheaper, and more reliable than trying to satisfy a specialist lender.

Why Hampshire Properties Are Particularly Affected

Hampshire has a high concentration of spray foam properties for specific reasons.

Southampton and Portsmouth’s post-war housing estates — built across Shirley, Bitterne, Woolston, Paulsgrove, and Leigh Park through the 1950s, 60s, and 70s — were heavily targeted by energy efficiency grant schemes in the 2000s. Many homeowners in these areas received spray foam through council-coordinated programmes with little understanding of what was installed.

Winchester’s older Victorian and Edwardian properties are frequently found to contain spray foam applied by contractors as a roof repair shortcut. New Forest properties face additional complications from National Park planning considerations if remedial roof work follows removal.

Portsmouth and Hayling Island coastal properties face elevated moisture risk — the Solent environment accelerates the damage spray foam causes to roof timbers.

The Only Thing That Clears a Lender Refusal

Professional removal with a lender-accepted completion certificate.

There is no negotiation with lenders on this point. What they require:

- Written confirmation that all spray foam has been professionally removed

- Structural assessment of roof timbers confirming their condition

- Photographic evidence of the cleared roof space

- Professional credentials and memberships of the removing contractor

This document — issued after removal — is what clears the lender flag and allows your mortgage or remortgage application to proceed.

What Happens to Your Hampshire Property Value Without Removal

A Hampshire property with spray foam insulation is effectively only sellable to cash buyers. Cash buyers know this — and they price accordingly, typically offering 25–40% below market value to account for the removal cost and risk.

On a Hampshire property valued at £350,000, that discount represents £87,500–£140,000. Professional removal costs a fraction of that.

Frequently Asked Questions

Will removing spray foam definitely get my Hampshire mortgage approved?

In the vast majority of cases, yes — provided removal is carried out professionally and a proper completion certificate is issued. The certificate is what lenders need to see. A small number of lenders may still require additional surveyor sign-off, but professional removal with full documentation resolves the issue for most mainstream lenders.

My Hampshire surveyor flagged spray foam — how quickly can it be removed?

Most standard Hampshire residential properties complete within one to two days. We provide a free online estimate first so you know the scope and cost before committing.

Does the type of foam affect which lenders will consider my Hampshire property?

Yes. Open-cell foam gives you slightly more options with specialist lenders if paperwork exists. Closed-cell foam is refused by virtually every mainstream and specialist lender regardless of condition. A survey confirms which type you have.

Can I remortgage my Hampshire property after spray foam removal?

Yes — once removal is complete and a completion certificate is issued, you can resubmit to mainstream lenders including Halifax, Nationwide, Barclays, and Santander. Most Hampshire remortgage applications proceed without further issues after professional removal.

Does spray foam affect equity release in Hampshire?

Yes. Every equity release provider in the UK refuses properties with spray foam. Removal is the only option if you want to access equity release on your Hampshire property.

If spray foam is blocking your Hampshire mortgage, remortgage, or equity release, the first step is a free online estimate.