Surrey homeowners are discovering a problem that nobody warned them about when the spray foam was installed.

Whether it was put in under the Green Homes Grant, suggested by an insulation company, or installed years ago as a quick energy-saving fix — the result is the same. Surveyors are flagging it. Mortgage lenders are refusing applications. Sales are collapsing. And the homeowner is left dealing with the consequences.

This guide explains what is happening, why Surrey properties are particularly affected, and what your options are right now.

Why Is Spray Foam a Problem for Surrey Homeowners?

Surrey has some of the highest property values outside central London. Towns like Guildford, Reigate, Woking, Esher, and Weybridge attract buyers who are almost always purchasing with a mortgage — and that is exactly where the problem starts.

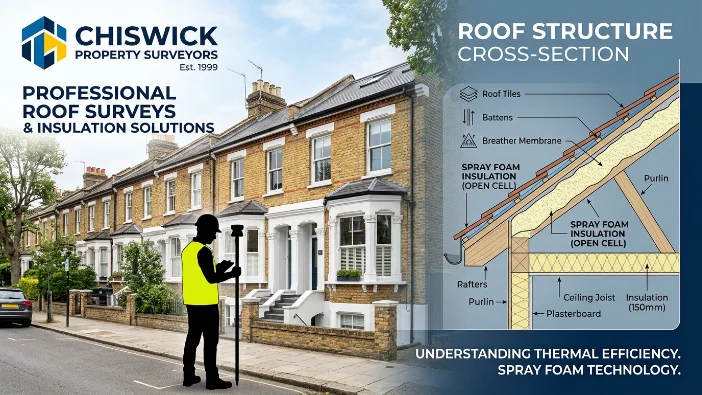

When a buyer’s mortgage lender sends a surveyor to assess a Surrey property, the surveyor needs to inspect the roof structure. They need to see the timber rafters, check the condition of the felt or membrane, and confirm the roof is in a sound state.

Spray foam makes that impossible. It covers everything — rafters, tiles, membrane — in a solid layer that cannot be looked through. The surveyor cannot confirm the condition of what is underneath. Without that confirmation, most lenders will not proceed.

In Surrey, where properties are high value and most transactions rely on mortgage lending, this is a serious problem. A lender refusing to lend does not just affect one buyer — it collapses the entire transaction, potentially pulling apart a chain that other people are depending on.

Which Surrey Lenders Are Refusing Mortgages?

This is not a small number of cautious lenders. The list covers virtually every major bank and building society operating in Surrey.

Halifax, Nationwide, Barclays, NatWest, Santander, TSB, and Skipton Building Society are among the lenders who flag or refuse applications on properties with spray foam insulation in the roof space. TSB in particular has taken one of the most straightforward positions — they will not lend on spray foam properties at all.

Equity release lenders are even stricter. If you own a Surrey property and were planning to release equity to fund retirement, home improvements, or care costs, virtually every equity release provider will decline while spray foam is present.

A small number of specialist lenders may consider applications, but they typically charge higher rates, require additional surveys, and many still refuse at the end of the process.

Surrey Properties — Why the Risk Is Higher Here

Surrey’s housing stock has several characteristics that make the spray foam problem more acute here than in other parts of the country.

Older housing stock. Towns like Dorking, Reigate, and Guildford have significant numbers of Victorian and Edwardian properties. These homes were designed to breathe — their roof structures rely on natural airflow between tiles and timbers to manage moisture. Spray foam eliminates that airflow completely, which in older properties dramatically increases the risk of condensation and timber decay.

High property values. The average Surrey home is worth significantly more than the national average. When spray foam causes a sale to fall through or forces a price reduction, the financial impact on the homeowner is proportionally larger.

Active mortgage market. Surrey’s commuter belt location means high transaction volumes and a constant flow of buyers relying on mortgage lending. More transactions means more surveys — and more opportunities for spray foam to be flagged.

Period properties and conservation areas. Many Surrey villages contain listed buildings and properties in conservation areas. These properties often have traditional timber roof structures that are particularly vulnerable to moisture damage when ventilation is blocked by spray foam.

What Happens When Spray Foam Is Flagged in a Surrey Survey?

The scenario plays out the same way for most Surrey homeowners.

An offer is accepted. The buyer arranges a mortgage. The lender sends a surveyor. The surveyor spots the spray foam and flags it in their report. The lender either refuses outright or puts the application on hold pending further investigation.

At that point, the buyer has a problem — and so does the seller.

In some cases, buyers walk away entirely. In others, they use the survey finding to renegotiate the price downward — knowing the seller’s options are limited. Cash buyers who are willing to proceed typically factor the removal cost into their offer, reducing what the seller receives.

Estate agents across Surrey are now routinely advising sellers to address spray foam before listing, rather than discovering the problem mid-transaction when the pressure is highest and the options are fewest.

Does Spray Foam Actually Damage Surrey Properties?

Not always immediately — but the risk is real and it increases over time.

The core issue is ventilation. Traditional Surrey roofs, particularly in older properties, are designed as cold roofs — air circulates between the tiles and the insulation layer in the loft floor, keeping the roof timbers dry. When spray foam is applied to the underside of the roof, that ventilation is sealed off.

Moisture that would previously have escaped now has nowhere to go. It condenses against the timbers. Over years, this creates conditions for damp, mould, and eventually timber decay.

The Property Care Association and Home Owners Alliance found that 35% of properties inspected had at least one defect caused by spray foam insulation, based on surveys of over 500 properties. In Surrey’s older housing stock, that figure is likely to be at least as high — possibly higher, given the age and construction of many properties.

The properties that do not yet show damage may develop it. And surveyors, knowing this risk, will flag spray foam regardless of whether visible damage has occurred.

Can You Sell a Surrey Property With Spray Foam?

Technically yes — but your options are limited and the price impact is real.

Without removal, you are selling to cash buyers only. In Surrey’s property market, that significantly reduces the pool of potential buyers. And those buyers know your situation — they know you cannot sell to mortgage buyers, and they will use that to push the price down.

If you want to sell at full market value, to any buyer, without complications — removal is the practical route.

What Is the Solution?

Professional spray foam removal restores your roof to a condition that surveyors and lenders can work with. Once removal is complete, you receive written documentation confirming the work has been carried out. That documentation is what your lender or buyer’s solicitor will need before proceeding.

At Spray Foam Removal UK, we work with Surrey homeowners regularly — across Guildford, Reigate, Woking, Epsom, Leatherhead, Dorking, Farnham, and throughout the county. Our spray foam removal service in Surrey covers the full process from initial survey through to completion certificate.

How Much Does Spray Foam Removal Cost in Surrey?

Costs vary depending on the size of the property and the type of foam installed.

As a general guide for Surrey homeowners:

| House Type | Open-Cell Foam | Closed-Cell Foam |

|---|---|---|

| Terraced | £2,500 – £3,000 | £3,000 – £3,500 |

| Semi-Detached | £3,000 – £3,500 | £3,500 – £4,000 |

| Detached | £3,500 – £4,200 | £4,200 – £5,000+ |

Closed-cell foam costs more to remove because it is denser and bonds more aggressively to roof surfaces.

The best way to understand your specific costs is to start with a free estimate based on your property details.

FAQs

My Surrey home had spray foam installed under a government scheme is anyone responsible for the removal cost?

The government’s position is that homeowners should seek redress from their installer in the first instance. In practice, many homeowners find this route difficult or unavailable, and end up covering the cost themselves. There is currently no government financial assistance for removal.

Will removal definitely fix my mortgage problem?

In most cases, yes – professional removal with the correct documentation allows lenders to reassess your application. Lender decisions are always their own, but removal with a completion certificate resolves the issue for the majority of Surrey homeowners who go through the process.

How long does removal take for a typical Surrey property?

Most jobs take between 2 and 5 days. If you have a sale or remortgage deadline, removal can usually be scheduled to fit your timeline.

Do I need a survey before removal?

In most cases, yes — a survey confirms the foam type and the condition of the roof structure, which shapes the removal approach and final cost. Some straightforward cases can be quoted without a full survey.

What happens to the loft after removal?

The loft will need re-insulating with a lender-approved alternative — mineral wool rolls or PIR boards are the most common choices. These are breathable, mortgage-friendly, and typically cheaper to install than spray foam was.

Spray foam does not have to stop your Surrey sale or mortgage application.

Most of our customers get a quote within 24 hours. No obligation, no pushy sales calls — just a clear picture of what removal involves and what it costs.