Hampshire homeowners are running into a problem that is stopping property sales dead in their tracks.

The spray foam insulation that was installed in the loft — sometimes years ago, sometimes under a government-backed energy efficiency scheme — is now causing mortgage surveyors to flag the property, lenders to refuse applications, and buyers to walk away.

If you are trying to sell a Hampshire property and this has happened to you, you are not alone. And there is a clear path through it.

What Is Going Wrong With Hampshire Property Sales?

The process usually follows the same pattern.

A seller accepts an offer. The buyer arranges a mortgage. The lender sends a surveyor to inspect the property. The surveyor goes into the loft, sees spray foam on the underside of the roof, and flags it in their report.

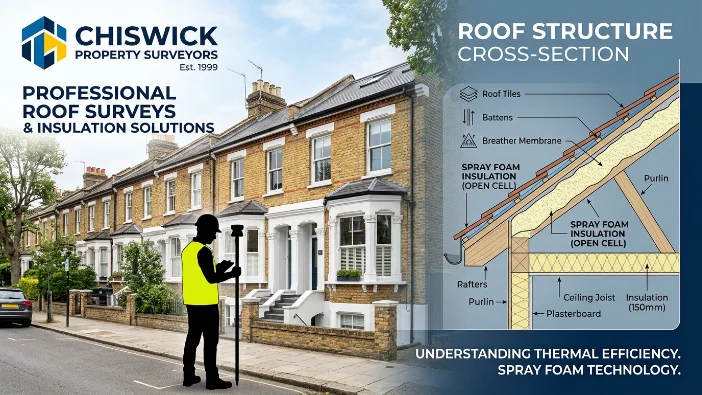

From that point, most lenders will not proceed. They need to be able to assess the condition of the roof timbers before they will lend against the property. Spray foam makes that impossible — it covers the rafters, tiles, and membrane in a solid layer that cannot be inspected without removal.

The transaction stalls. In many cases, it collapses entirely.

Estate agents across Hampshire — in Southampton, Portsmouth, Winchester, Basingstoke, Fareham, and across the county — are now seeing this happen regularly. Some are advising sellers to address spray foam before listing, rather than discovering the problem mid-sale when the options are limited and the pressure is high.

Why Hampshire Properties Are Particularly Affected

Hampshire has a broad and varied housing stock, and several factors make spray foam a particularly acute problem here.

The Green Homes Grant. Between 2020 and 2022, the government’s Green Homes Grant provided vouchers of up to £10,000 to fund insulation upgrades. Spray foam was among the insulation types funded under the scheme. Hampshire had a significant number of installations under this and related programmes — meaning a large number of local properties now have spray foam that was put in relatively recently, before the mortgage implications were widely understood.

Older housing stock. Hampshire has a high proportion of older homes — Victorian and Edwardian terraces in Southampton and Portsmouth, pre-war semis across the county, period properties in market towns like Romsey, Alresford, and Petersfield. These homes were built to breathe. Their roof structures depend on natural airflow to manage moisture. When spray foam seals off that ventilation, the risk of condensation and timber decay rises significantly.

Strong buyer demand and mortgage reliance. Hampshire’s combination of coastal towns, commuter access to London, and quality of life makes it an active property market. Most buyers in the county are purchasing with a mortgage — which means most transactions go through a surveyor, and most surveyors are now trained to flag spray foam.

The Impact on Your Sale Price

Even if a sale does not collapse entirely, spray foam affects what you can realistically achieve.

Cash buyers — the only buyers who can purchase without a mortgage survey blocking proceedings — are a small part of the market. And cash buyers know your situation. They know you cannot sell to mortgage buyers without removing the foam first. That knowledge gives them significant negotiating power, and they will use it.

Realistic cash offers on spray foam properties in Hampshire are typically well below market value. The buyer is pricing in the cost of removal and the inconvenience of dealing with the issue themselves.

If you want to sell at full market value, to any buyer, without the transaction being derailed at survey stage — removal before listing is the practical answer.

Which Lenders Are Refusing Hampshire Mortgages?

The list of lenders flagging or refusing spray foam properties covers virtually every major bank and building society in the UK.

Halifax, Nationwide, Barclays, NatWest, Santander, TSB, and Skipton Building Society are among those with policies that flag spray foam as a mortgage risk. TSB has taken one of the clearest positions — they will not lend on spray foam properties.

For Hampshire homeowners looking at equity release, the picture is even bleaker. Virtually every equity release provider will decline applications on properties with spray foam present, regardless of condition.

What About Properties Where the Foam Was Installed Correctly?

This is a fair question — and one that many Hampshire homeowners ask.

The government’s position is that spray foam installed in line with the relevant standards should not prevent a mortgage. In practice, this has not changed lender behaviour. Most lenders are not satisfied by installation certificates or guarantees. Their concern is not just whether the foam was applied correctly — it is that they cannot independently verify the condition of what is underneath it. Until someone physically removes the foam and confirms the roof structure is sound, lenders will not proceed.

The Property Care Association and Home Owners Alliance found that 35% of properties inspected had at least one defect caused by spray foam, based on inspections at over 500 properties across the UK. That figure is significant enough that lenders treat all spray foam properties with caution — regardless of how the installation was done.

Can You Remove Spray Foam Before Listing in Hampshire?

Yes — and for most homeowners in this situation, that is exactly what we recommend.

Addressing spray foam before your property goes on the market means:

- No mid-sale collapses caused by a surveyor flagging it

- No forced renegotiation from buyers using it as leverage

- A clean, mortgage-ready property that any buyer can purchase

- Full market value rather than a reduced cash offer

The removal process typically takes 2 to 5 days depending on property size and foam type. Combined with the time to arrange a survey and schedule the work, most Hampshire homeowners can have removal completed within 2 to 3 weeks of making first contact.

Find out more about our spray foam removal service in Hampshire.

How Much Does Spray Foam Removal Cost in Hampshire?

Costs depend on the size of the property and the type of foam installed.

| House Type | Open-Cell Foam | Closed-Cell Foam |

|---|---|---|

| Terraced | £2,500 – £3,000 | £3,000 – £3,500 |

| Semi-Detached | £3,000 – £3,500 | £3,500 – £4,000 |

| Detached | £3,500 – £4,200 | £4,200 – £5,000+ |

Closed-cell foam is more expensive to remove because it is denser and bonds more aggressively to roof surfaces. Open-cell foam is softer and typically quicker to work with.

The best way to understand your specific cost is to start with a free estimate based on your property details.

What Happens After Removal?

Two things follow professional removal.

First, your loft will need re-insulating. Lender-approved alternatives to spray foam — mineral wool rolls, blown cellulose, or PIR boards — are breathable, mortgage-friendly, and typically cheaper to install than spray foam was in the first place.

Second, you will receive written documentation confirming the removal has been professionally carried out. This is what your buyer’s solicitor, mortgage lender, or surveyor will need to see. Keep this document safely — it will be useful for any future sale or remortgage too.

FAQs

How do I know if my Hampshire property has spray foam?

The easiest way is to look in your loft. If the underside of the roof tiles is covered in a foam layer — either soft and spongy or hard and rigid — that is spray foam. If you are not sure, a professional survey will confirm it.

My property has spray foam from the Green Homes Grant — what are my options?

The government advises homeowners to seek redress from their installer in the first instance. If that route is not available, you may have recourse through TrustMark or an insurance-backed guarantee if one was issued at the time of installation. In practice, many homeowners find these routes difficult and end up paying for removal themselves.

Will removal guarantee my sale goes through?

Removal resolves the surveyor and lender concern in the vast majority of cases. Once removal is complete and documented, buyers’ lenders can proceed with a standard mortgage survey. Individual lender decisions are always their own, but removal with the correct documentation resolves the issue for the overwhelming majority of Hampshire homeowners who go through the process.

Can I claim the removal cost back from anyone?

Potentially — if the installer was at fault, you may have a claim under consumer protection legislation. Your first step would be to contact the installer directly. If they are unresponsive or no longer trading, TrustMark may be able to help. Legal advice from a solicitor specialising in property or consumer law would be the appropriate next step if other routes are exhausted.

Do I need to re-insulate straight after removal?

Not immediately — but you should not leave the loft uninsulated long-term. A bare loft space affects heat retention and will eventually affect your EPC rating. Most homeowners arrange re-insulation as part of the same project, or shortly after.

If spray foam is standing between you and your Hampshire sale, the sooner you address it the better.

Most of our customers get a quote within 24 hours. No obligation, no pushy sales calls — just a clear picture of what removal involves and what it will cost for your specific property.