If you have spray foam insulation in your Wiltshire loft, you may already know something is wrong. A surveyor has flagged it. A mortgage has been refused. A sale has stalled. Or perhaps you have just discovered it is there and want to understand what it means before problems arise.

This guide is written for Wiltshire homeowners who need clear, practical information. It explains what spray foam insulation mortgage problems actually are, why they affect so many properties across the county, and what your realistic options are right now.

What Is the Spray Foam Mortgage Problem?

Spray foam insulation is applied as a liquid that expands and sets solid inside a roof space. It was widely promoted as a modern, energy-efficient upgrade and was included in government schemes such as the Green Homes Grant and ECO4 programme. Thousands of Wiltshire homeowners had it installed, many without any warning about the mortgage implications.

The core problem is straightforward. When spray foam is applied to the underside of a roof, it covers the timber rafters, roof tiles, and breathable membrane in a solid layer. A surveyor sent by a mortgage lender cannot see through that layer. They cannot inspect the condition of the timber. They cannot confirm whether the roof is sound. Without that confirmation, most lenders will not proceed.

The result is that properties with spray foam insulation are increasingly being refused mortgages, declined for remortgaging, and rejected for equity release. In Wiltshire, this is affecting homeowners in Swindon, Salisbury, Chippenham, Trowbridge, Devizes, Warminster, Marlborough, Calne, and across the county.

Why Does Spray Foam Cause Such Serious Problems?

There are two distinct issues at play: structural risk and financial risk. Both matter.

Structural risk. Traditional Wiltshire roofs, particularly on older properties, are designed as cold roofs. Air circulates between the outer tiles and the insulation layer in the loft floor, keeping the roof timbers dry by allowing moisture to escape naturally. When spray foam seals the roof space, that ventilation is gone. Moisture builds up against the rafters. Over months and years, this creates conditions for condensation, damp, mould, and timber rot. Because the foam covers everything, the damage develops unseen. The Property Care Association and Home Owners Alliance found defects caused by spray foam in 35% of properties they inspected across the UK.

Financial risk. Lenders refuse spray foam properties not just because of the structural risk, but because they cannot independently verify what condition the roof is in. That uncertainty alone is enough for most lenders to decline. It does not matter how well the foam was installed. Most lenders will not proceed until it is removed and the roof structure is confirmed as accessible and sound.

Which Lenders Are Refusing Mortgages in Wiltshire?

The list of lenders with policies that flag or refuse spray foam properties is extensive.

Halifax, Nationwide, Barclays, NatWest, Santander, TSB, and Skipton Building Society are among the major lenders with such policies. TSB has taken one of the clearest positions and will not lend on spray foam properties at all. For equity release, virtually every provider in the UK will decline applications on properties where spray foam is present, regardless of whether the foam was professionally installed or government-funded.

Even when homeowners have installation certificates or guarantees, lenders are still refusing. The paperwork does not resolve the underlying issue, which is that the roof cannot be inspected.

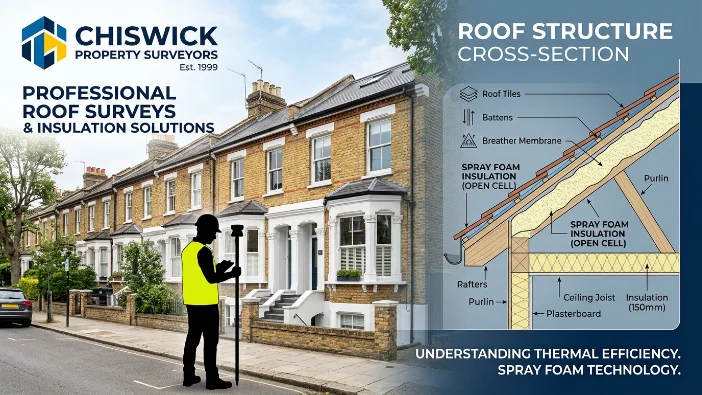

Open-Cell and Closed-Cell Spray Foam: What You Need to Know

Not all spray foam is the same, and the type in your loft affects both the risks and the removal cost.

Open-cell spray foam is soft and spongy. Press it with your finger and it springs back. It is more breathable than closed-cell, which means it allows some moisture movement. The structural risk is lower, but it still covers the roof structure and prevents inspection. Most lenders will still flag it.

Closed-cell spray foam is completely rigid. It feels like hard plastic and does not compress at all. It seals the roof space completely, blocks all ventilation, and bonds directly and aggressively to tiles, rafters, and membrane. The structural risk is significantly higher, and the removal process is more complex and more expensive.

If you are not sure which type you have, checking is straightforward. Go into your loft and press the foam. Soft and springy is open-cell. Hard and immovable is closed-cell. If you cannot safely access your loft, a professional survey will confirm it.

Can You Sell a Wiltshire Property With Spray Foam?

You can try, but the practical difficulties are significant.

Without removing the foam, you are limited to cash buyers only. In Wiltshire’s property market, where most buyers use mortgage lending, that dramatically reduces your pool of potential buyers. Cash buyers who are willing to purchase a spray foam property understand the situation. They know you cannot sell to mortgage buyers without removing the foam first, and they will use that to negotiate the price down.

Properties with spray foam in Wiltshire regularly sell for less than their true market value, or do not sell at all when listed without removal. Estate agents across the county are now advising sellers to address spray foam before going to market, rather than discovering the problem mid-transaction when a buyer’s mortgage has been refused and the pressure is at its highest.

What Does Professional Spray Foam Removal Involve?

Removal is specialist work. It is not something that can be done safely or effectively as a DIY project.

Spray foam bonds to roof tiles, rafters, and breathable membrane. Forcing it off without the right technique and equipment breaks tiles, tears the membrane, and can split the timber rafters beneath. That structural damage costs more to repair than the removal would have cost in the first place. And even if you manage to physically remove the foam yourself, you will not produce the completion documentation your lender needs. A DIY removal does not generate a certificate. It leaves you with a damaged roof and no paper trail.

Professional removal follows a structured process. A specialist surveys the loft first, confirming the foam type, coverage, thickness, and the current condition of the roof structure. On the day of removal, respiratory protection and dust containment are set up before any foam is touched, because spray foam dust contains isocyanates that must be managed properly. The foam is then worked away from the roof surface carefully using specialist tools, protecting tiles and timber throughout. All foam waste is removed and disposed of correctly under UK environmental regulations. The loft is left clean, clear, and ready for a surveyor to inspect. Written documentation confirming professional removal is then issued.

That completion documentation is what your lender, buyer’s solicitor, or equity release provider will ask to see. It is the evidence that the job has been done properly and that the roof structure is now accessible.

Find out more about our spray foam removal service in Wiltshire and how the process works from first contact through to completion certificate.

How Much Does Spray Foam Removal Cost in Wiltshire?

Costs depend on property size and the type of foam installed.

| House Type | Open-Cell Foam | Closed-Cell Foam |

|---|---|---|

| Terraced | £2,500 – £3,000 | £3,000 – £3,500 |

| Semi-Detached | £3,000 – £3,500 | £3,500 – £4,000 |

| Detached | £3,500 – £4,200 | £4,200 – £5,000+ |

Open-cell foam removal costs less because the foam is softer and generally quicker to detach. Closed-cell foam is denser and bonds more aggressively, making it more time-consuming and more expensive to remove.

For most Wiltshire homeowners, the cost of removal is significantly less than the financial impact of either selling at a reduced cash-buyer price or being unable to sell or remortgage at all.

What Happens After Removal?

Once the foam has been professionally removed, two things follow.

Re-insulation. Your loft will need new insulation. Lender-approved alternatives including mineral wool rolls, PIR boards, or blown cellulose are breathable, mortgage-friendly, and typically less expensive to install than the spray foam was in the first place. They also support a healthy EPC rating, which matters both for selling and for ongoing running costs.

Timber inspection. With the foam removed, the condition of the roof timbers becomes fully visible. If moisture has been present for years, there may be signs of damp or early timber decay that were hidden beneath the foam. Minor issues are usually straightforward to treat. More significant damage will require timber repair or replacement before re-insulation. Your removal specialist will advise on what they find.

Frequently Asked Questions

How long does spray foam removal take for a Wiltshire property?

Most jobs take between 2 and 5 days depending on property size, foam type, and loft access. From first contact to receiving your completion certificate, most Wiltshire homeowners have the issue resolved within 2 to 3 weeks.

My foam was installed under the Green Homes Grant or ECO4. Who pays for removal?

The government’s position is that homeowners should seek redress from their installer in the first instance. In practice, many Wiltshire homeowners find this difficult, particularly where the installer is no longer trading or disputes responsibility. There is currently no government financial assistance for removal costs. Some homeowners have recourse through TrustMark or an insurance-backed guarantee if one was issued at the time of installation.

Will removal fix my mortgage or sale problem?

In the vast majority of cases, yes. Professional removal with the correct completion documentation allows lenders to reassess. The overwhelming majority of homeowners who go through the removal process properly find that their mortgage application, remortgage, or property sale can then proceed.

Is spray foam removal covered by home insurance?

In most cases, no. Removal is generally classed as a remedial or maintenance job rather than an insured event. It is worth checking your specific policy, but most standard home insurance policies do not cover the cost of elective removal.

I am not planning to sell for several years. Do I still need to think about this?

If you have no plans to sell, remortgage, or release equity in the near future, the situation is less urgent. However, it is worth understanding what type of foam you have and monitoring the condition of your loft space over time. Moisture problems from closed-cell foam in particular can develop slowly and cause structural damage that becomes expensive to address later.

If spray foam insulation is affecting your Wiltshire property, getting a clear picture of your situation is the first step.

Most of our customers get a quote within 24 hours. No obligation, no pushy sales calls. Just a clear picture of what removal involves and what it will cost for your specific property.